|

TUESDAY EDITION June 9th, 2026 |

|

Home :: Archives :: Contact |

|

|

The BTC, Oil Prices and A War in the CaucasusDave Cohendave.aspo@gmail.com Monday, 18 August 2008 The direct use of force is such a poor solution to any problem, it is generally employed only by small children and large nations. Recent events in the Caucasus and Turkey remind us that choke points in world oil transit are subject to geopolitical disruption. Operator British Petroleum (BP) was forced to shut down the Baku-Tbilisi-Ceyhan (BTC) pipeline after a terrorist attack in Turkey that occurred 2 days before the Russian military incursion into Abkhazia, South Ossetia and Georgia (hurriyet.com.tr). The BTC has a capacity of 1 million barrels per day (b/d) and carries Azerbaijani oil destined for Europe from Baku to the port of Ceyhan on the Mediterranean Sea (map below). The BTC is used to deliver light crude oil from the large Azeri-Chirag-Gunashli field in the Caspian Sea.

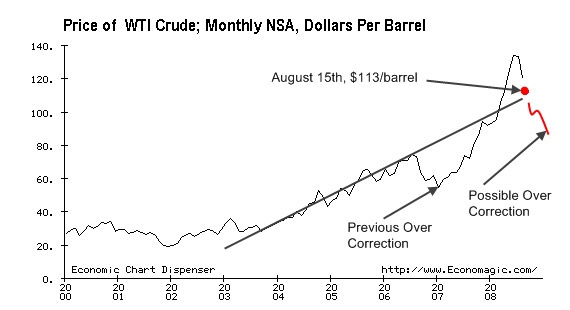

Two insights arise from this disruption of Caspian oil supplies. I'll discuss each one below. Oil Price MovementsIt is amazing that the BTC shutdown had little discernible effect on oil prices, which have been falling precipitously for over a month now. Despite the disruption to global oil supplies, the price of sweet light crude dropped yesterday [August 11] by 75 cents to $113.70 a barrel. Julian Lee, senior energy analyst with the Centre for Global Energy Studies, said: “It is quite remarkable that the world has lost one million barrels [per day] but the market has not really been bothered. It shows a fundamental shift in market perceptions.” What it shows, Julian, is that an irrational herd mentality has seized the oil markets and no temporary event affecting supply & demand fundamentals can dent bearish sentiments at this time. Even oil inventories, which are in the lower part of their historical range, have not persuaded traders to bid up oil. All of this is quite the opposite of an equally irrational bullish sentiment that seized the markets in the run-up to $147/barrel. If the BTC had been shut down during the bulllish phase, prices could easily have jumped up $10 or more in a single day. Other factors have lowered the price, including the latest dollar rally and the mysterious end of speculation by Morgan Stanley, Goldman Sachs and others, who were investing in oil futures at the same time that they were also forecasting higher prices, which had the desired effect of further driving up those prices. Actually, the speculation is simply going in a different direction; bearish traders are selling oil short now betting that the price will fall.1 And of course, large volumes of shut-in oil count for nothing when you've got put options (The Australian, August 14, 2008)— The market may have limited upside, however. As futures plunged, many traders took out puts, or options to sell, when oil hit various prices between $US120 and $US100 a barrel. Those options expire later this week [ending today], creating a natural resistance in the market to moving much higher than its latest settlement. Oil price movements show meaningful trends over periods counted in years, not days or weeks or even a few months. Here's the latest version of what is rapidly becoming my favorite graph—I have finally learned that effective information marketing requires constant repetition.

The gray trend line reflects the supply & demand fundamentals over a 5 year period. Lately, those fundamentals seem to be undergoing a small but significant shift because world oil demand appears to have fallen a bit as a result of the exuberant price run-up—oil traders are presently sold on this shift. Unfortunately, the data, outside of weekly EIA reports, is too sketchy to allow us to draw any definite conclusions. The China demand data is clouded by preparations for the Olympics, and European total oil products demand appears to be flat (IEA). If a significant demand shift has indeed occurred, this might imply a slight flattening of the 5-year supply & demand trend, assuming OPEC continues to pump oil at record rates. That's a big IF. Should oil fall below $100/barrel, it is likely OPEC will start cutting production. Thus we will likely re-live the skyrocketing price nightmare we saw earlier in 2008 sometime later this year or in 2009. So it goes. In the past I have tried to emphasize that the harmful effects of peak oil will take many years to unfold. For those predicting oil prices falling back to $50/barrel (Barrons) or those saying prices of $500/barrel are possible in 3 to 5 years (Robert Hirsch), I would suggest that the truth lies somewhere in the middle. If I'm right, extrapolate the gray trend line (graph above) to see where prices are headed in coming years. The Barrons view is based on an unrealistic view of supply and a misapplication of historical price cycles which no longer pertain in the peak oil era, while the Hirsch view is based on an unrealistic view of demand, which would be utterly "destroyed" long before oil reached $500/barrel or even $300. My own view is laid out in The Prognosis for the United States (ASPO-USA, June 25, 2008). Russian Hegemony and the BTCThere is some scary talk coming out of Russia concerning the autonomy of Georgia and the fate of the BTC pipeline (hurriyet link op. cit.). An adviser to the Russian parliament also claimed the closed pipeline would not be opened again and declared the line is "dead". "The world and countries in the region have seen that not NATO, but Russia is the only one who could secure the energy routes," Alexander Dugin, international politics advisor to the Russia's Duma, told Turkish Cumhuriyet daily. "In this context, regarding Turkey's energy politics, it should be said that the BTC is not running at the moment and it will not run again." Actually, the BTC will likely re-open next week but if it does not, one would hope that NYMEX oil traders will take note that as much as 850,000 b/d has been physically removed from the world market—this is far more oil than the recent U.S. consumption cuts. Russian troops "shelled" the BTC this week. The Wall Street Journal reports that "a neat row of large craters in a field in southern Georgia strongly suggests that Russia dropped bombs near oil and gas pipelines bringing fuel to the West." Georgian officials say Russian warplanes dropped bombs in an early Saturday raid close to the Baku-Tbilisi-Ceyhan pipeline, which pumps some 850,000 barrels of crude a day -- or 1% of total global oil demand -- from Azerbaijan to the Mediterranean. The bombs narrowly missed the line, but one exploded just 10 feet away from it. You don't always have to hit the target to make your point. Russia's (Putin's) re-assertion of their traditional hegemony in the Caucasus may signal that Caspian oil is at risk not only now, but in all the years to come. This is bad news because Caspian oil is one of the few sources outside of OPEC that can provide steady or increased production in future years. But after the mauling Georgia got, "any chance of a new non-Russian pipeline out of Central Asia and into Europe is pretty much dead," says Chris Ruppel, an energy analyst at Execution, a brokerage in Greenwich, Conn. The risk of building a pipeline through countries vulnerable to the wrath of Russia is just too high. Putin runs a large risk if he attempts to shut down the BTC permanently, an action that would throw the oil markets into chaos. Russia has already demonstrated that they are an irresponsible actor in the natural gas markets, but the oil markets have been exempt up to now. Ruppel is no doubt correct when he says that additional pipelines carrying Caspian oil outside of Russian control are no longer an option.

Contact the author at dave.aspo@gmail.com Notes 1. In the case of stock, "short sellers borrow stock and sell it, betting the price will drop. If their bet is correct, they can buy new shares later at a lower price, repay the borrowed stock, and pocket the difference between the sale price and the repurchase price." |

| Home :: Archives :: Contact |

TUESDAY EDITION June 9th, 2026 © 2026 321energy.com |

|

As crude oil gets more and more precious in upcoming years, strategic geopolitical moves to control a larger share of that oil will become more frequent. Putin (pictured left) has forcefully made his point about who will control the Caucasus. But before President George W. Bush further condemns Russia for invading Georgia, he would be well advised to ask himself who invaded Iraq. Small children and big nations—they tend to act alike.

As crude oil gets more and more precious in upcoming years, strategic geopolitical moves to control a larger share of that oil will become more frequent. Putin (pictured left) has forcefully made his point about who will control the Caucasus. But before President George W. Bush further condemns Russia for invading Georgia, he would be well advised to ask himself who invaded Iraq. Small children and big nations—they tend to act alike.{kind=link}