|

TUESDAY EDITION June 9th, 2026 |

|

Home :: Archives :: Contact |

|

|

Enhancing Energy Security to Sustain Economic Growth and Development: Interview with Nobuo Tanaka, Executive Director, International Energy Agency (IEA)Interview by Keith W. Rabin Nobuo Tanaka took over as Executive Director of the IEA in September 2007. Previously, he had been Director for Science, Technology and Industry at the Paris-based Organization for Economic Co-operation and Development (OECD). Mr. Tanaka began his career in 1973 in the Ministry of Economy, Trade and Industry (METI) in Tokyo. Mr. Tanaka first joined the OECD in 1989 as Deputy Director of the Directorate for Science, Technology and Industry, and was promoted to Director in 1992. In 1995, he returned to METI and served in a number of high-ranking positions, the most recent being Director-General, Multilateral Trade System Department, Trade Policy Bureau. In the energy field, Mr. Tanaka was responsible for Japan’s involvement with the IEA and the G7 Energy Ministers’ Meeting during the second oil crisis. In the late 1980s, he helped to establish the comprehensive energy policy of Japan and oversaw the implementation of Japan’s international nuclear energy policy and negotiation of bilateral nuclear agreements. Mr. Tanaka worked on formulating international strategy as well as coordinating domestic environment policy and energy policy in the Kyoto COP3 negotiation. He was Minister for Industry, Trade and Energy at the Embassy of Japan, Washington DC from 1998-2000. Mr. Tanaka, has a degree in Economics from the University of Tokyo and an MBA from Case Western Reserve University, Cleveland, Ohio. Interview by Keith W. Rabin

Hello Tanaka-san. It is good to see you again. Before we begin can you tell our readers a bit about your background and how you came to lead IEA? I served in the Japanese government at the Ministry of Economy, Trade and Industry for many years dealing mostly with international trade and energy issues. Much of my career has been spent outside of Japan. Several years ago I came back for my second assignment with the OECD in Paris. The head position at IEA opened and I was asked to run as a candidate. It was an interesting time for energy security and climate change issues and I was elected as the first non-European Executive Director. I started in September 2007 just before the price of oil started to escalate dramatically. In 2008 it rose as high as $147 per barrel and it was almost like we experienced a third oil shock. Then it came down dramatically before it resumed its ascent. So there has been a lot of volatility during my time here, and it has been an interesting experience and challenge.

Can you tell us about the role of IEA in international energy markets and its history?

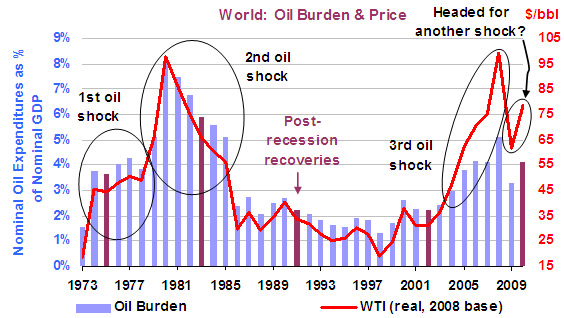

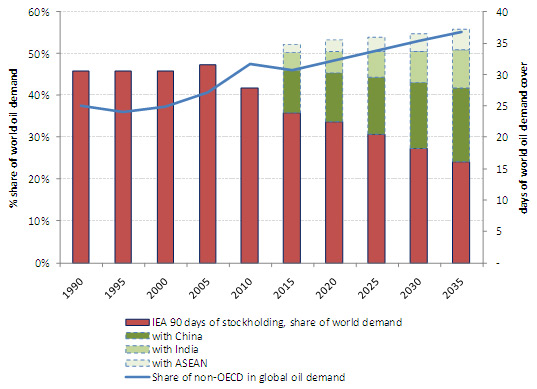

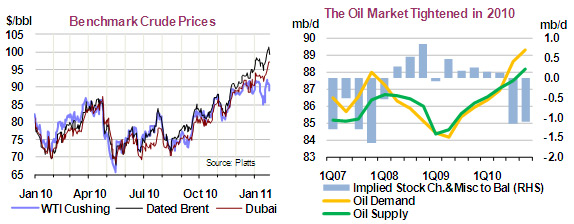

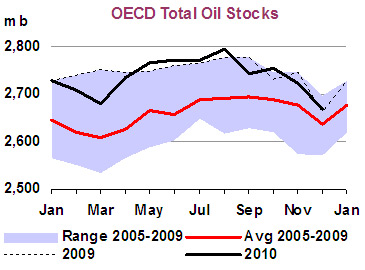

The IEA was established in 1974 at the time of first oil shock as consuming countries united to face the OPEC production cartel. The objective was to promote stability in the oil market through creation of a strategic stockpile. Currently there are 28 countries, each of which has a mandate of holding 90 days of their previous year’s imports. Our mission is to analyze the petroleum market and in case of emergency decide how much we need to release jointly to cool down the market. IEA stockholding cover of global oil demand In fact we have utilized this mechanism only two times. The first was in 1991 during the first gulf war when Iraq invaded Kuwait. The second was in 2005 when Hurricane Katrina hit the Gulf of Mexico. But this is an important function. When oil prices spike up, knowing it is there alleviates some pressure in the market even if we do not have to use it. With Brent crude now approaching $100 a barrel the market is getting tighter due to more positive trends developing in the global economy. So if we get disruptions and spikes due to unexpected factors we have this capacity in place to help alleviate any potential disruptions. The IEA's 2010 World Energy Outlook forecasts with current policies the average price of a barrel of oil will exceed $100 in the next few years and by 2035 the effective price will exceed $150. Can you explain this as well as the "New Policies" and "450 Scenario" forecasts which could help to limit these increases?

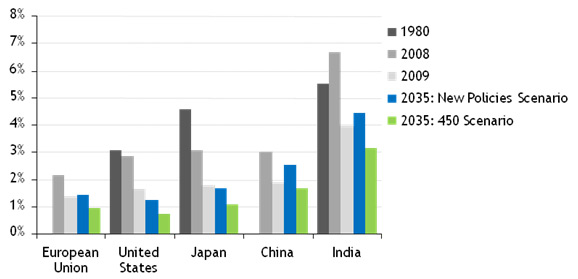

Oil-import bills as share of GDP in selected countries The third “450 Scenario” is based mostly on pledges announced in association with the Copenhagen Accord, as well as plans to remove fossil fuel subsidies. These reductions would require international agreement on a structured framework of policies as well as their implementation. Under this alternative, prices would go to $98 and then come down gradually. Achieving this alternative would also require a large increase in infrastructure investment. Do current events in Egypt and the Middle East affect this thinking? Of course the current situation has an impact on the price of oil. We view price movements to be impacted by various signals to the market, and since last autumn there has been a 30% increase in the price of oil. In hindsight we can see much of this has been caused by increases in demand in emerging as well as developed markets. Seasonal factors and weather also play a role. It is important, however, to determine what is a long-term trend and what is a temporary phenomenon. For example, many Chinese provinces reduced coal use last year and turned to diesel to realize 20% increases in energy efficiency targets. That increased seasonal demand, which is temporary, and caused supply to become tighter toward end of year.

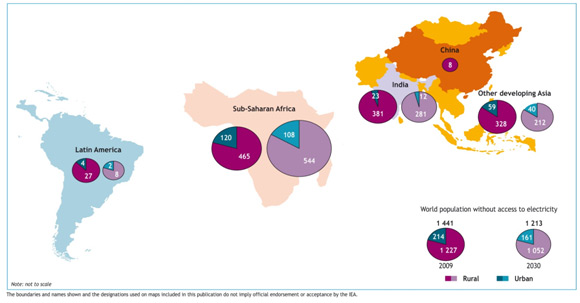

As a result, stockpiles became lower and some OPEC countries raised production. This lowered free capacity, and we are cautious at this price level. If a $100 price continues for most of the year, we calculate the “Oil Burden” (Global Oil Expenditures divided by Global GDP) will exceed that of 2008, a year of abnormally high prices. If that happens this could undermine the global economic recovery. It is also problematic that this burden is much higher in emerging economies such as India or in Africa, and affects the poor in these societies. What are the underlying factors driving these price rises? Is it more a "peak oil" scenario where we are exhausting existing supply, consumption increases in emerging markets, a failure to finance exploration activity, or a combination of these concerns? Additionally, how do you respond to analysts who believe most of the volatility we see is the result of speculators and hedge funds than real supply factors and fundamentals? The economic recovery that has begun to take hold is increasing demand and the market is tightening. But we don’t deny that financial speculation does have an impact. The weaker dollar and recent political risk in countries such as Tunisia and Egypt certainly have an effect, which amplifies volatility, but in the end we think fundamentals are the primary driver. The trend is then accentuated by financial factors and the activities of investors and speculators, both on the upside and then when it turns down. Number of people without access to electricity (million) Oil prices have stayed quite strong in recent years despite the economic downturn. This leads one to wonder what the current price for oil would be if we were seeing stronger growth in the developed world. Wouldn't the higher prices that result from stronger growth act as a tax and impinge on the sustainability of a recovery? We tend to take the consensus view from international organizations such as OECD and IMF as we are not macroeconomic forecasters ourselves. For 2011 we assume 4.3%. That is � % slower than 2010 and we are worried about the state of the global economy in the face of rapidly rising commodity prices.

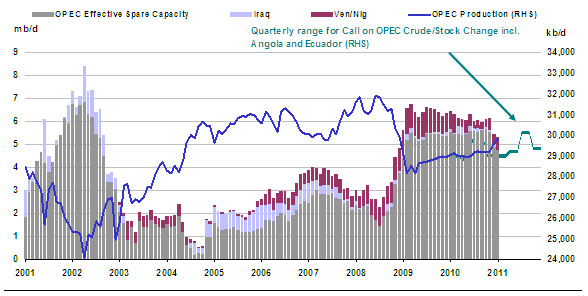

At the same time we see far more spare capacity in OPEC and the OECD than what we saw in 2008. For that reason we think we have more of a buffer this year compared to that time. We also know there are geopolitical tensions that could potentially disrupt the market but do not see any reason to panic. At the same time, we cannot be complacent and need to maximize development both of new sources of energy as well as the policies needed to increase efficiency, alternatives and movement toward realization of our 450 scenario or a similar scenario.

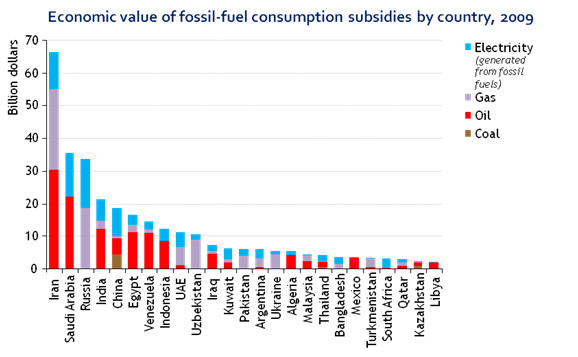

One of the main challenges facing energy and resource markets is the very different needs and concerns of developed versus developing economies. This is particularly problematic when we talk about global warming as well as energy efficiency issues. How can these differences be resolved in a way that addresses both the needs of the emerging world as well as overall global and environmental concerns? All countries need to contribute if we are to successfully tackle climate change. This is especially true of major players such as China and the US. Without them it is just impossible. Each country has different priorities. For example in some oil producing countries many still have much cheaper domestic gasoline prices due to fossil fuel subsidies when compared to exports. This sends a very wrong signal. They will be big consumers going forward – and we think they need to phase out the subsidies. We estimate fossil fuel subsidies amounted to $300 billion in 2009. That is huge and if a phase out happens we can save 2 gigatons of emissions and 5 million barrels of oil. This would be a big contribution and we strongly support this kind of action. In consuming nations better efficiency standards, greener building codes and development of alternative energy sources and supporting infrastructure are all important. For China, which became the largest energy consumer in 2009, much needs to be done in terms of efficiency and development of cleaner coal and carbon capture. So each region and country needs to contribute to mitigate the damage. We can only succeed if everyone contributes their fair share.

We hear a lot of talk about the importance of alternative energy yet wind, solar, hydro, biofuels and geothermal are unlikely to serve as a significant replacement to petroleum for many decades. What is your view on the development of alternative energy sources both over the long term and the next few decades?

We don’t agree that they will play a minor role as renewables already play a major role in many markets starting in Europe, the US and China. There have also been significant increases in investment even in the midst of a major economic downturn. We see renewables having a 32% share of power generation by 2035 and if we are able to move to our 450 scenario this will go up to 45%. That is a major increase. Costs are dropping rapidly for solar and other technologies and this will continue with more research and experience. So governments need to adopt the right policies and adjust their support systems. Valuation of carbon needs to be more transparent and steady and reflect true values and costs. Renewables also need to be integrated into the system and a smart grid developed and financed. Technology development is important but market design and policies are also critical elements to support this transformation. In contrast to alternative energy most analysts recognize the immediate viability of nuclear as a power source. What is your view on nuclear as an energy source both in developed countries as well as emerging markets?

For those countries that allow nuclear this is very important. Some countries, especially in Europe are negative, though others such as France and Finland endorse it. The issue is public acceptance and governments need to provide information, maintain safety and address nonproliferation concerns so this technology can be more fully utilized. As we seek to transition to alternative energy there is concern developing over its reliance on rare earth and other specialty metals. Some analysts believe we are merely trading our reliance on hydrocarbons to these inputs. What is your view on this and how can we resolve this problem?

There are energy-reliant appliances and vehicles that use these metals as part of their process but in the end it is primarily a matter of cost rather than supply -- at least over the long term. Several IEA countries possess deposits of these specialty metals, and some have mothballed mining capacity that may cost a bit more to exploit than imports from foreign suppliers -- which is why these facilities ceased operations in the first place. But the deposits are ready to mine, and so IEA countries are therefore not reliant on these suppliers for rare earths over the longer term, in the way for example that they are increasingly reliant for oil imports on those with significant reserves. Given rising concerns over energy and resource supplies we are seeing political concerns emerge largely driven by economies that are nervous about potential disruptions. This is leading to diplomatic tensions, investments into supply by sovereign wealth funds, attempts by energy and commodity-producing countries to renegotiate production and exploration agreements with multinationals and other private companies, and resistance to allowing investments that would place these real assets in the hands of foreign corporations. How much of a concern are these developments and what are the implications moving forward? There are plenty of resources underground and the risk of peak oil seems mainly to be above ground. This is due to resistance by national governments and limits in exploration budgets and longer term capital investment. Macondo Commission Report implies Delays & Higher Costs

Under our long term scenario we see three price assumptions but in each case consumer prices remain high. In the 450 scenario it is $90 per barrel of oil, but countries have to add the cost of carbon emissions on top of that. As a result, the real financial cost is almost as high as the $150 per barrel seen in the “business as usual” scenario. As a result we can say the age of cheap energy is over -- regardless of which scenario emerges. That is something businesses and government need to recognize and then take steps to diversify technologies and capacity to enhance and address energy security. These measures are important both for growth and development as well as for climate change and security. Ultimately, the use of energy and its resulting environmental impact is a global issue with global implications. At the same time given the difficulties and perceived ineffectiveness of operating on a multilateral basis, we are seeing increased movement toward national, bilateral and regional approaches. Is this perception fair? How important is multilateral cooperation in resolving energy concerns and what can be done to increase cooperation moving forward?

When we calculate the domestic actions of countries like China they are significant. Interestingly it is often far easier for countries to act locally than to commit themselves formally within a global framework. That is often overlooked. So when we aggregate what is being done it is significant and if the desired progress is achieved it will lower what they need to do globally. Mexico is also doing more domestically with their forests, energy efficiency and other programs. Thank you Tanaka-san for your time and attention. Before we conclude do you have any final words you would like to leave with our readers? That is all for now. Thanks and look forward to speaking again soon. Interview by Keith W. Rabin |

| Home :: Archives :: Contact |

TUESDAY EDITION June 9th, 2026 © 2026 321energy.com |

|

Our annual outlook evaluates trends in the energy market and outlines scenarios for the future. It is not a forecast. In 2010 we constructed three alternatives. “Business as Usual” reflects current policies and under this scenario we see oil going to $150 a barrel in constant 2009 dollars. We believe that is the necessary price to balance current supply and demand factors. Under the “New Policy” scenario, which we view as likely, governments will focus on introducing measures to promote energy efficiency, conservation and a greater reliance on renewables. In this case we think it will rise to $113, also by 2035.

Our annual outlook evaluates trends in the energy market and outlines scenarios for the future. It is not a forecast. In 2010 we constructed three alternatives. “Business as Usual” reflects current policies and under this scenario we see oil going to $150 a barrel in constant 2009 dollars. We believe that is the necessary price to balance current supply and demand factors. Under the “New Policy” scenario, which we view as likely, governments will focus on introducing measures to promote energy efficiency, conservation and a greater reliance on renewables. In this case we think it will rise to $113, also by 2035.

Nuclear is a very important part of the global energy portfolio. It is low carbon and relatively cheap compared to other sources. To reach our 450 scenario, thirty new nuclear plants need to be built each year until 2035.

Nuclear is a very important part of the global energy portfolio. It is low carbon and relatively cheap compared to other sources. To reach our 450 scenario, thirty new nuclear plants need to be built each year until 2035.

Multilateral cooperation is indeed important. After Copenhagen and Cancun there has not been a global agreement but our view is we can’t wait for a global deal as that will take time. And if we wait the cost of mitigation and addressing important energy and climate issues will get higher and higher. For example, we calculate the cost of enacting measures pledged in the Copenhagen accord would require $1 trillion to achieve the 450 scenario and the cost gets higher and steeper by 2020 as we get closer to the target year of 2035. As a result we participated in the Clean Energy Ministerial meeting in Washington last July and called for action in these areas. Countries know what they have to do and have established goals. They need to start as soon as possible so this kind of “bottom-up” approach can help achieve progress until a global accord can be developed.

Multilateral cooperation is indeed important. After Copenhagen and Cancun there has not been a global agreement but our view is we can’t wait for a global deal as that will take time. And if we wait the cost of mitigation and addressing important energy and climate issues will get higher and higher. For example, we calculate the cost of enacting measures pledged in the Copenhagen accord would require $1 trillion to achieve the 450 scenario and the cost gets higher and steeper by 2020 as we get closer to the target year of 2035. As a result we participated in the Clean Energy Ministerial meeting in Washington last July and called for action in these areas. Countries know what they have to do and have established goals. They need to start as soon as possible so this kind of “bottom-up” approach can help achieve progress until a global accord can be developed.