|

TUESDAY EDITION June 9th, 2026 |

|

Home :: Archives :: Contact |

|

|

Suez Weekly Market Monitor

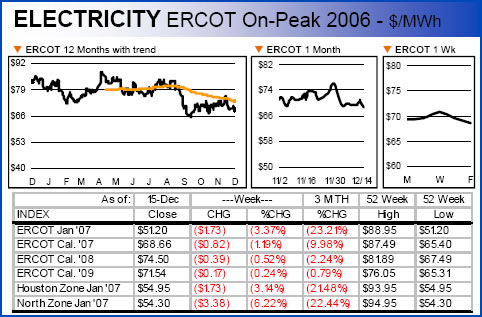

Derek Mumford ERCOT Power ERCOT power stayed in sync with the natural gas market, following the static trend in the early week, with a mid-week bubble and declining prices for the remainder.

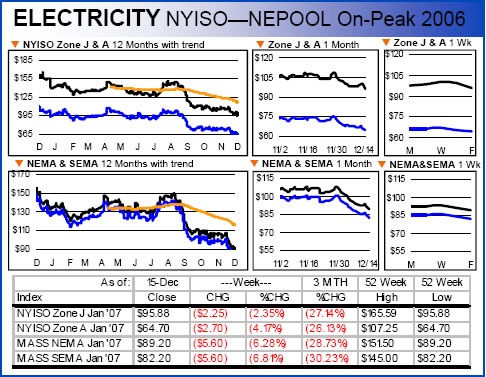

NYISO—NEPOOL Power Northeast power prices matched the natural gas curve with prices climbing mid-week then gradually falling off hitting new 52-week lows in the reported zones.

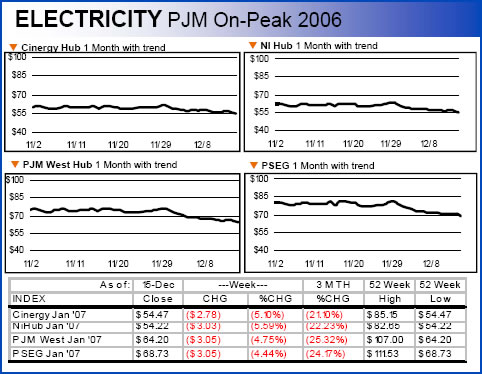

PJM Power PJM power prices for the reported zones reached new 52-week lows as gas prices fell last week.

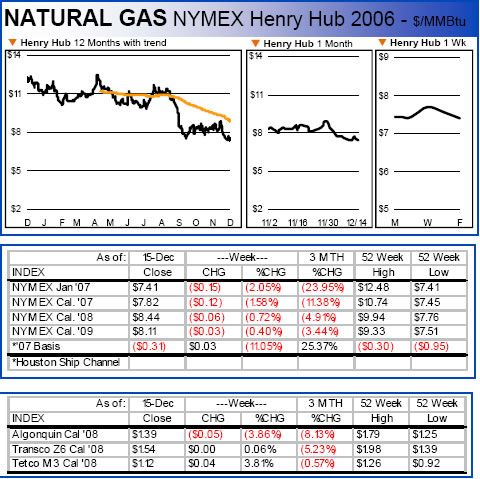

Natural Gas Market Natural gas prices were static in the early part of the week. Prices spiked midweek then gradually declined.

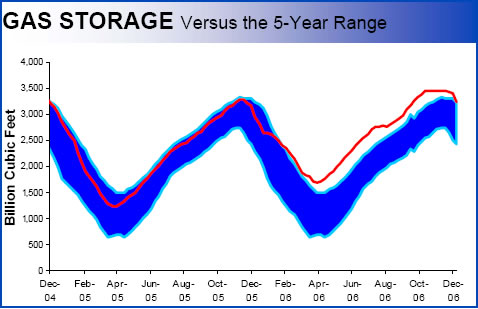

Natural Gas Storage: Gas in Storage Decreased 168 Bcf

Working gas in storage was 3,238 Bcf as of Friday, December 8, 2006, according to EIA estimates. (Source: EIA) International Energy Outlook Non-Organization for Economic Co-operation and Development (OECD) Europe and Eurasia and the Middle East account for almost three-quarters of the world’s natural gas reserves, but in 2003 they accounted for only 39 percent of world production. Together, these two regions account for 47 percent of the projected increase in global natural gas production from 2003 to 2030, much of it for export to OECD countries. Russia is already the world’s single largest exporter of natural gas, with net exports of 6.3 trillion cubic feet in 2003, all of it by pipeline. There are also some plans to export natural gas from the Middle East, but much of the region’s increase in production is projected to be used domestically—particularly in the electric power sector, where shifts from petroleum to natural gas allow the producing countries to monetize more of their oil assets through export. Natural gas production in non-OECD Asia also grows substantially over the projection period, but all the growth in supply is required for consumption within the region, and imports are needed to fill the shortfall. In Central and South America, natural gas production outpaces regional demand. As a result, Trinidad and Tobago continues to export LNG outside the region. Peru, and possibly Venezuela, may also begin to export LNG outside the region over the course of the projection. In 2003, the OECD countries accounted for 41 percent of the world’s total natural gas production and 52 percent of total natural gas consumption; in 2030, they are projected to account for only 25 percent of production and 40 percent of consumption. Natural gas supply from the OECD nations increases by an average of only 0.5 percent per year in the IEO2006 reference case, whereas demand increases by 1.5 percent per year. As a result, the OECD countries rely increasingly on imports to meet natural gas demand, with a growing percentage of traded natural gas coming in the form of LNG. OECD countries rely on natural gas produced in other parts of the world to meet more than one-third of their natural gas consumption in 2030, up from 22 percent in 2003. LNG is expected to become an increasingly important source of supply to meet the world’s demand for natural gas. Although there were only 12 LNGexporting countries in 2004-6 the number is increasing. In 2005, Egypt joined the ranks of LNG producing countries with the start of two separate liquefaction projects. Russia also entered the LNG business in 2005, not with LNG it produced but with LNG for which it traded pipeline natural gas. Not until 2008, when the Sakhalin liquefaction project is expected to start operations, will Russia become an LNG-producing country. Norway and Equatorial Guinea also have their first liquefaction terminals under construction, and construction on the first liquefaction terminal in South America is scheduled to begin in 2006 in Peru. The number of countries installing the infrastructure necessary to accept LNG imports is also increasing. More than 30 years had passed since the United Kingdom imported LNG, but in 2005 it rejoined the ranks of LNG importers, with the startup of its Isle of Grain regasification terminal. China, Canada, and Mexico all have their first LNG import terminals under construction; and Germany, Poland, Croatia, Singapore, and Chile are among the other countries considering their first regasification terminals. (Source: EIA)

Derek Mumford |

| Home :: Archives :: Contact |

TUESDAY EDITION June 9th, 2026 © 2026 321energy.com |

|