|

THURSDAY EDITION June 4th, 2026 |

|

Home :: Archives :: Contact |

|

|

The Big Picture

John J. Riley April 25, 2005 This past month the performance of the stock and bond market was…. I’m sorry, I’m not going to talk about this past month or even this year. This report is going to give you a perspective that you might not have seen before. It is going to be about the next 10, 20 even 30 years. It is going to be about the Big Picture. We invest into the future. Having a clear vision of the future makes investing easier and helps to eliminate some of the worries about short-term bumps in the road. The focus is going to be on oil and how it will effect virtually everything. In doing the research for this report I found out that a number of popular beliefs were false and the facts are much more interesting and more importantly, predictable. First, I want to make it clear, we are not likely to ever run out of oil. But that doesn’t mean production won’t decline in the future and it doesn’t mean that all of the oil in the ground is useable oil. Secondly, the problems listed in this article are also opportunities for the investor wise enough to benefit from them. By knowing the economic landscape ahead of time gives us the advantage we need to be able to prepare and plan. Problems are only problems for those that don’t plan ahead. Information

sources Its

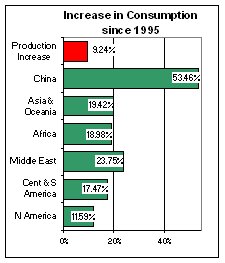

All About Consumption I say “experts” because the conventional wisdom from Wall Street has been that the consumption rates of these regions would top out years ago. It hasn’t and it is not likely to for many years, even decades to come. Urbanization/Development

Drive Consumption The UN estimates that over the next 45 years, the population of Africa is expected to double. Asia is likely to see an increase of about 34%, Latin America and the Caribbean about 39%. The developing regions have a shift going on internally from rural to urban. City life requires the consumption of more energy. These shifts and consumption increases are going on right now. Production

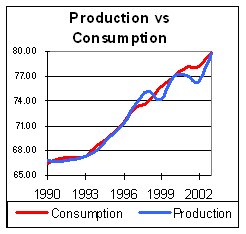

Can’t Keep Up Can’t

They Just Pump More Oil? Pumping oil out of the ground is not as simple as turning on a faucet. After a certain point, an oil field hits its peak production and then the amount of oil production steadily declines. There are ways to increase the production, but most cause the decline to sharpen. Slow, steady extraction is the best way to get most of the oil. Hubbert’s

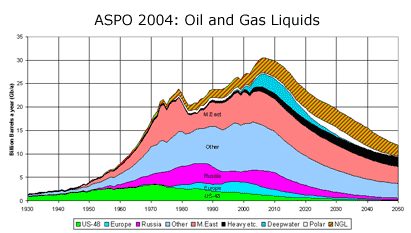

Peak and Peak Production From

1949 through the 1960’s, an oil industry geophysicist named M.

King Hubbert wrote important research papers that His research showed that the US peak would happen in the early 1970’s (it did) and global oil production would peak sometime early in the 21st century. The exact date of his prediction of the global oil peak is irrelevant. What is more important is to understand it may be already happening. There is evidence all around us. Peak production does not mean the oil field has run dry. For various reasons, it gets harder and harder to pump oil out of the ground as an oil field ages. Technology

Actually Making Things Worse Think of it like the reverse of concrete being poured into a foundation. The concrete is very soupy, but still they pour it slowly and have workers all around the foundation poking deep into the cement to insure that there are no air pockets and that the cement fills the space completely. Oil

production is the same in reverse. It has to be extracted slowly to

insure that Disturbing

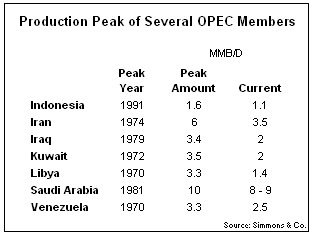

Lesson From Oman Production, thanks to technology, peaked at 250,000 bbl/day by 1997. By 2001, production was down to 90,000 bbl/day. 2004 estimates are around 40,000 bbl/day. What is worse is that Yibel is now expected to produce less than half of the original estimate of the oil in the ground. Simmons says the event took everyone by surprise, that it “came out of the blue”. It shouldn’t have though. All of the warning signs were in place. Are

there other Yibel’s out there? The answer is an unqualified yes.

Peak

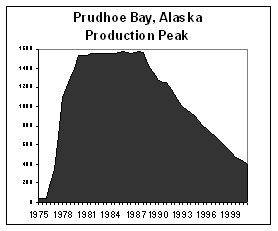

Production Has Already Happened to Many Oil Fields Other oil fields that we think of as bottomless have declined in recent years. 2002 production from some fields in the North Sea are down about 90% from their peaks about 20 years ago. Prudhoe Bay in Alaska is down about 60% from its peak in the late 80’s. Old

Oil Fields Few

New Finds Increasing

Consumption + Declining Production = ??? We know the trend, we know the factors, but how much will a developing, powerful nation like China or India be willing to pay? Because, like it or not, we believe they will be determining the future price of oil, not the developed world. What

Does This Mean to Investors? Inflation/Deflation We expect to see a disconnect between corporate bonds and Government bonds as corporates under-perform a market we already expect to do poorly. Stock

Market Opportunities Other

Resources Conclusion The future for oil as an investment continues to be excellent. But not just oil, as the developing world continues to grow, many other natural resources and commodities will be effected in the same way. The Dollar doesn’t look so good, but that is great for foreign stocks and bonds. And even the negative for the US stock market is an opportunity for those that understand how to benefit from a market decline though hedges. We will still be looking for short term breaks in the market, but we believe any pull-back in oil or hard assets will be short-lived and a buying opportunity.

Questions, comments, further information, to Cornerstone Investment Services,

LLC John J. Riley

Securities offered through Cantella & Company, Inc.,

Member, NASD, SIPC No warranty or guarantee is given regarding

the accuracy, reliability, veracity, or completeness of the information

provided here or by following links from this page, and under no circumstances

will the author or service provider be liable for any loss including but

not limited to direct, indirect, incidental, special or consequential

damages caused by using the information, or as a result of the risks inherent

in the stock market. The information contained herein is for informational

purposes only and is not a solicitation to buy or sell any investment.

Copyright © 2004 Cornerstone

Investment Services, LLC |

| Home :: Archives :: Contact |

THURSDAY EDITION June 4th, 2026 © 2026 321energy.com |

|

view from the inside.

view from the inside.  consumption

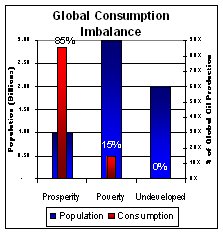

needs, according to Simmons & Co., currently 1 billion people (Prosperity)

use 85% of the world’s oil. There are 5 billion other people in

the world. 3 billion (Poverty) use the remaining 15% of the world’s

oil. As these 3 billion develop, moving from poverty to prosperity,

their consumption (of everything, including oil) will sky-rocket. Even

if their consumption grows to only 1/3 of the consumption of the prosperous,

per capita, oil production would have to double. And that doesn’t

include the remaining 2 billion people not using any energy yet.

consumption

needs, according to Simmons & Co., currently 1 billion people (Prosperity)

use 85% of the world’s oil. There are 5 billion other people in

the world. 3 billion (Poverty) use the remaining 15% of the world’s

oil. As these 3 billion develop, moving from poverty to prosperity,

their consumption (of everything, including oil) will sky-rocket. Even

if their consumption grows to only 1/3 of the consumption of the prosperous,

per capita, oil production would have to double. And that doesn’t

include the remaining 2 billion people not using any energy yet.  that

shows by 2010 global demand for oil is expected to be about 93 Mmb/day

(Million Barrels/Day). Non-OPEC sources of oil are expected to be about

49Mmb/day. This leaves 44Mmb/day for OPEC. They are currently pumping

about 30Mmb/Day. Best estimates are that OPEC could increase their production

by about 4 Mmb/Day. This leaves a 10Mmb/Day shortfall.

that

shows by 2010 global demand for oil is expected to be about 93 Mmb/day

(Million Barrels/Day). Non-OPEC sources of oil are expected to be about

49Mmb/day. This leaves 44Mmb/day for OPEC. They are currently pumping

about 30Mmb/Day. Best estimates are that OPEC could increase their production

by about 4 Mmb/Day. This leaves a 10Mmb/Day shortfall.  detailed

the coming oil production peak and decline. His research has been accepted

by major oil companies, oil industry associations and the auto industry

as realistic.

detailed

the coming oil production peak and decline. His research has been accepted

by major oil companies, oil industry associations and the auto industry

as realistic.  all of the oil from all of the little pockets is gotten. The faster

the oil is pumped out, the more likely there will be oil left behind.

This oil then becomes unrecoverable.

all of the oil from all of the little pockets is gotten. The faster

the oil is pumped out, the more likely there will be oil left behind.

This oil then becomes unrecoverable.

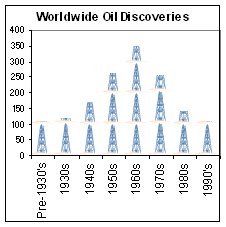

year since the 1960’s. There haven’t been any “Giants”

found since then either. Most new finds have been small. The deep water

oil, Russian oil, Caspian Sea Oil and Canadian sand oil have all proven

to be either more hype than reality or extremely difficult and expensive

to extract.

year since the 1960’s. There haven’t been any “Giants”

found since then either. Most new finds have been small. The deep water

oil, Russian oil, Caspian Sea Oil and Canadian sand oil have all proven

to be either more hype than reality or extremely difficult and expensive

to extract.