|

TUESDAY EDITION June 9th, 2026 |

|

Home :: Archives :: Contact |

|

|

Mr. Market Gets It Wrong AgainDave Cohendave.aspo@gmail.com May 29th, 2009 Now do you want to hear some real bullishness? Crude has fallen

so far, so fast, that we could see a snap-back rally drive it to $62 …

$77 … heck, even $90 is possible! Once again the price of oil is in La La Land. Today the price of NYMEX light sweet crude surged past $62/barrel. My best guess based on the supply & demand fundamentals is that crude should not be trading a penny over $35 per barrel right now. In a justified fit of pique last December I wrote The Price Is Not Right, which attempted to get to the bottom of why oil prices move up or down. Today’s essay is Not Right, Part II. I now believe oil has not been priced “correctly” for the last 34 months going back to about July, 2006. Exceptions to the new rule crop up because even a broken clock tells the right time twice a day. Why does Mr. Market get it wrong over and over again? Green Shoots Raise the Oil Price?

GDP in the European Union shrank 2.5% in 2009:Q1. It was down 4.6% year-over-year. Recent Wall Street Journal reports included these observations.

Oil demand strength can be viewed as following from economic

conditions. However, due to its tight correlation with GDP, demand also

serves as an indicator of those conditions. World oil demand is way

down. Japan, where GDP shrank 15.2% in 2009:Q1, consumed 3.57 million barrels-per-day in March, down 1.45 million barrels compared with previous year. For the week ending May 8th, demand in the United States was 18.194 million barrels-per-day,

down 1.56 million barrels (-7.9%) compared with the same week in 2008.

That’s 3 million barrels-per-day right there, and I’ve only listed 2

countries.

According to Platts, China consumed 6.69 million barrels-per-day in the 2009:Q1, down 4.5% over the previous year. The lone “bright spot” was India, which was up 4.8% averaged over the entire year 2008-2009 ending March 31st (2.65 million barrels-per-day). The sagging demand picture is clear enough. Although some of the quoted data is behind current conditions, key indicators say the global economy has not improved. So-called “green shoots” refer to a slowing of the rate of various declines. In a CNBC interview, economists Nouriel Roubini and Harvard economist Ken Rogoff explain why even a weak economic recovery is still months away. Roubini issued his standard warning—

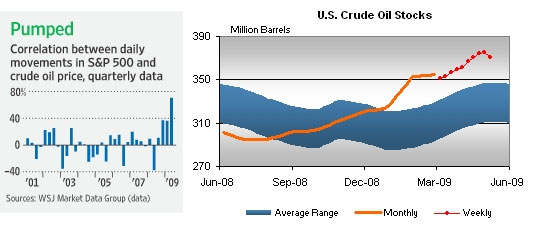

Howard Davidowitz tells Yahoo’s Tech Ticker why the worst is yet to come. Davidowitz provides a realistic assessment of wealth lost and debt de-leveraging that will take many years to achieve. Given the dismal demand numbers, why has the the price of crude been going up lately? The Wall Street Journal’s Liam Denning weighed in on the problem. Figure 1 shows the correlation between the oil price and movements in the S&P 500 along with the current inventory data from the EIA.

Figure 1 — The correlation with the S&P 500 (left) from the WSJ. Current inventories (crude stocks, right) from the EIA. Prices have risen as inventories remain far outside their 5-year average range. Note the slight downturn lately.

Two kinds of “green” have pushed the oil price up to heights it should never have attained lately: 1) a bogus perception of green shoots in our staggering economy; and 2) an influx of money into both equities (e.g. stocks) and crude oil. These factors explain the price differential between today’s $62 and my guestimate of the “correct” price (~$35 per barrel). The difference is necessarily unrelated to supply & demand fundamentals. This kind of oil market distortion has been going on for quite some time now, but with different causes at different times. Ignorance Is Not Bliss

Ponder the following two graphs and their captions.

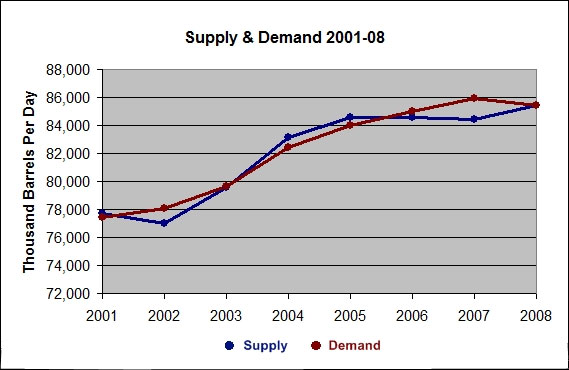

Figure 2 — World liquids supply & demand annual numbers for 2001-2008. Demand exceeds supply in 2006. The gap widens in 2007. Source data from the EIA (supply and demand).

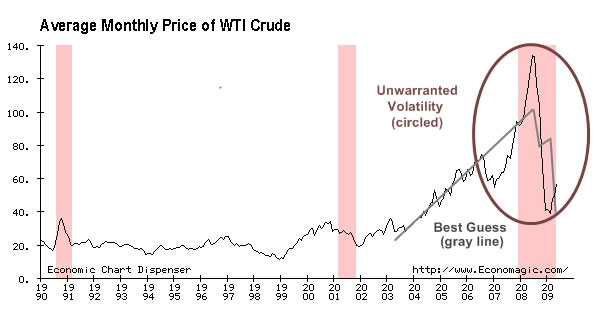

Figure 3 — Nominal WTI average monthly prices (NYMEX) 1990-present. The circled price series demonstrates unwarranted volatility (i.e. crazy price swings) after 2006:Q2. The gray line is my smoothed best guess of how the price should have moved during this period. Like a broken clock, the nominal line meets the gray line on occasion. What set the oil price adrift after 2006:Q2? Before turning to causes, let’s examine Mr. Market’s erratic history between then and now.

Let me take a moment to explain why oil prices reflecting actual market conditions might be important to us. Regardless of whether we are in the Peak Oil Era—we probably are—in 2009, we would like to know at all times what the relative abundance of the Elixir of Life—with respect to demand for it—of Industrial Civilizations is. Oil is important mainly because of our need to move people and stuff around. And please do not tell me about the latest biofuels & electric cars fantasy. The price signal is the traditional Way of Knowledge for gauging oil’s relative abundance measured in barrels produced daily to meet our needs. An accurate price signal helps us set priorities and plan for the future in almost all areas of life. But if Mr. Market is stoned, we do not know where we stand. Ignorance Is Bliss does not apply when it comes to oil’s availability and price. Index Fund Traders Bet On Oil

The Wall Street Journal’s Liam Denning believes the “oil [price] is really floating on cheap money” as investors in oil funds push up futures prices. This is the only reasonable interpretation of what’s going on. Reuters’ John Kemp supports Denning’s view.

I want to frame these observations in terms of supply & demand. Speculators betting on a long-term price rise by purchasing near-term contracts and rolling them forward, or physical traders buying oil now and storing it in tankers, are creating artificial demand for oil. This has everything to do with futures prices (the contango) and little to do with end-user demand (refiners). It has still less to do with inventory levels, which have actually gone down lately (Figure 1) because oil stored on tankers does not go into crude stocks. Thus the oil price goes up as the glut on the world market grows. Mr. Market is said to be behaving “correctly.” The contango is waning as the market “self-corrects”—the once steep differential between future and front month prices flattens out as current spot prices catch up with futures prices (Bloomberg, May 5, 2009). After the correction it is no longer advantageous to buy oil now and store it on tankers. Already Bloomberg reports that Shell failed to sell a load of North Forties crude.

Physical traders storing oil will start dumping it back on the market. They will need to dump it all or pile up losses leasing supertankers. The ensuing snowball will cause the oil price to crash. Oil may fall below its February low as today’s distorted $62 price becomes tomorrow’s distorted $25 price. I could be wrong of course. Mr. Market may experience another drug-induced mood swing which reflates the oil price. Naturally it is hard to predict Mr. Market’s future emotional state. How would you like to be an small independent oil exploration & production company trying to plan new drilling projects under these circumstances? There’s also the bandwagon problem I discussed in Not Right, Part I. We have all these “retail” investors who have no idea what they’re doing making the same mistakes together. Inexpert investors move in herds. I believe they’re about to lose their shirts, which will only make the price outlook worse when they head for the hills. Jump on in! The water’s fine! (said the sharks…) Why has the oil market become the playground of index fund traders? Why does the oil market follow the S & P 500? When my friends ask me (”the expert”) why the price of gas is going up during a recession, what I am supposed to tell them? I should tell them the allure of easy money broke the oil market and it has not been repaired. Perhaps the market is FUBAR and can’t be repaired. And Then There’s Stupidity

A bunch of smart people got together at the EIA’s 2009 annual conference to figure out what pushed prices upward in the first half of 2008. The cause of 2008’s crude price surge remains elusive according to conference participants (Oil & Gas Journal, April 9, 2009, subscription required). Nine months after crude oil prices reached record levels, experts agreed at the US Energy Information Administration’s 2009 annual conference on Apr. 7 that speculators shouldn’t be blamed. They also could not say definitively what pushed prices upward during 2008’s first half… Well, Jeffrey, if you think the market is functioning normally now, as you probably do, then I guess you won’t find any smoking guns. Generally speaking, if a person can’t see a hand being waved in front of his face, he’s going to miss a lot of things. All defenders of Mr. Market—they are legion—have the same eyesight problem. Robert F. McCullough Jr., managing partner at McCullough Research in Portland, Oregon, argued that the CFTC data is incomplete and uses “outmoded classifications that do not reflect the current make-up of the commodities market.” Harris responded that “the commission actually has begun to receive fairly good data from over-the-counter markets, especially about index funds, to supplement its own findings.” (Good to know!) Everybody agreed that supply & demand fundamentals were not to blame (see Figure 3). Everybody agreed the 2008:H1 price spike was inexplicable. Conference participants occasionally wandered into territory which (perhaps accidentally) overlaps reality.

I can already hear the protests. I have defamed the sacred market. The market does what the market does. The price of oil is the price of oil. The market can’t make mistakes by definition. My answer is Figure 3. Stare at this graph. Think really hard about it. Do those price movements since 2006:Q2 look right to you? The oil market is broken. Today’s $62 price makes no fundamental sense. As a friend told me, there’s trillions of dollars floating around out there and it’s got to go somewhere. Some of this moolah distorts the oil price. The explanatory burden falls on people who think Mr. Market is OK. Or the ones who think he’s a little woozy but can’t figure out why. Unless we get Mr. Market into rehab pretty damn quick, we are all going to pay the consequences. Contact the author at dave.aspo@gmail.com dave.aspo@gmail.comMay 29th, 2009 |

| Home :: Archives :: Contact |

TUESDAY EDITION June 9th, 2026 © 2026 321energy.com |

|