Is Natural Gas Cheap?

By David Galland

Casey Research

July 25th, 2009

At the height of its

late 2005 rally, natural gas in the U.S. was selling for just over $16/MMBtu, 350% higher than today’s price of $3.56.

The oil/gas ratio, now over 18, is an all-time high… suggesting that natural

gas is dirt cheap. So, it’s a buy, right?

In a phrase, not

exactly.

According to a recent report by Natural Gas Intelligence, U.S. natural

gas available for production “has jumped 58% in the past four years, driven by improved drilling techniques

and the discovery of huge shale fields in Texas, Louisiana, Arkansas and

Pennsylvania, according to a report issued Thursday by the nonprofit Potential

Gas Committee (PGC).”

According to the report, the increase in gas discoveries and

production improvements means that North America shouldn’t have to be concerned

about gas supplies for up to 100 years!

Dr. Marc Bustin provided an overview of the situation in the May edition of

Casey Energy Opportunities.

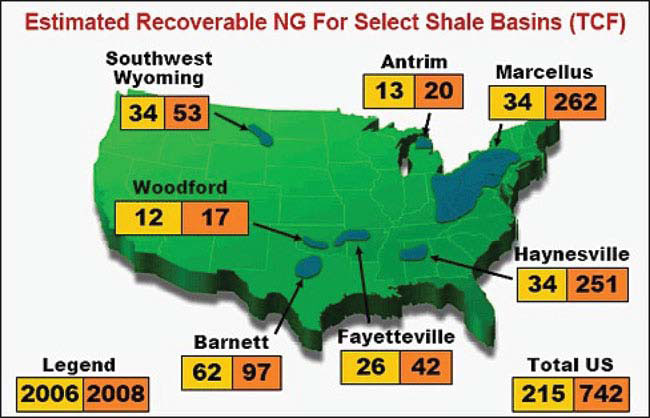

In the United States, the

tremendous growth in natural gas resources and estimated recoverable natural

gas, particularly from gas shales, just in the last two years (Figure 1) is

sending tremors through the entire industry. These tremors include the risk of

making obsolete the proposed $26 billion Alaskan and $16 billion northern

Canadian pipelines to tap northern gas resources and a slue of proposed LNG

terminals... unless they are for export!

The numbers currently kicked around are that something

around 2,000 trillion cubic feet of gas are technically recoverable in the

United States. At current production rates, this supply would last about 90

years.

Some analysts are predicting that even if the U.S. economy

recovers in the next year, the amount of gas discovered to date in gas shales

will severely dampen any increase in gas price for some time. According to a

new study by energy consulting firm CERA (Cambridge Energy Research Associates),

new technologies for unconventional gas fields are being applied so

successfully that supply is essentially no longer a driver in either production

or price in the North American gas market – whatever the market wants, North

American gas fields can supply. CERA reports that natural gas production in the

Lower 48 states has risen a startling 14% from 2007 to 2008, for example.

Figure 1. Major

shale areas or formations in the U.S. and the estimated recoverable natural gas

in 2006

and 2008. Modified from Daily Oil Bulletin (May 4, 2009).

Given the increase in production and the small slide in

demand, the price of natural gas has fallen to around $3.50-$4.00 per MMBtu

(down from $13 per MMBtu last summer). At these prices, many gas prospects are

uneconomic, and thus there has been a marked decline in the number of wells

being drilled. Rig activity (how many rigs are operating) is down about 50% in

North America.

But here is where an interesting feedback mechanism kicks

in. One of the characteristics of unconventional shale gas wells, and to a

lesser extent natural gas wells in general, is that the production rate

declines through time. Most shale wells’ production rates decline 60 to 90% in

the first year. If you were a gas company trying to survive amidst today's low

prices, the rate of return on your capital investment would also be painfully

low for a significant amount of gas if this were your initial year of

production.

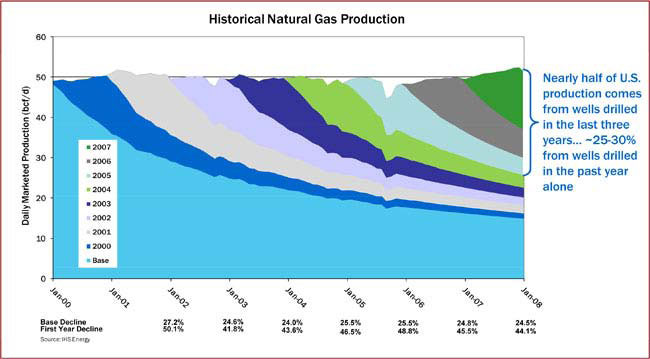

Another complementary fact is that over 50% of natural gas

consumed in the United States today is from wells drilled less than three years

ago, and 25-30% of the gas produced today comes from wells drilled last year

(Figure 2).

Hence it follows that if there are 50% fewer wells drilled

this year (from the drop in rig activity), new production will decline about

35-40% by the end of the year, so there will be gas shortages. Those will in

turn lead to higher North American prices, which in turn should lead to

additional drilling.

Figure 2. Historical

gas production in the U.S. showing the percentage of production from vintage of

well

(modified from Chesapeake April 2009 Investor presentation from original

data of HIS Energy)

Everything else being equal (which it's not, this being the

real, not the mathematical world), gas prices and drilling will see-saw until

an equilibrium is reached. In detail, of course, things are more complicated,

but it is pretty clear that gas prices will have to rise within the year, and

the big losers will remain the more expensive plays that require higher gas

prices to be economic.

Where will the gas price end up in the short term? A poll of

analysts by Reuters suggests $6 MMBtu in 2010 (Daily Oil Bulletin, May 4,

2009), but I don’t think I would bet on a gas price based on a vote by

analysts. At the same time, it's an interesting coincidence (or not –

coincidence, that is) that many prospects become economic at around the $6

MMBtu range. Among them are the Haynesville and Marcellus shales – and it's no

large leap from there to see their tremendous gas production potential acting

as a buffer to gas prices going much higher in the near term.

Thus, while there may

be some seasonal and relatively short-term trading opportunities in natural

gas, the overhang of ready supply places a fairly firm cap on the price. Which

begs the question, which big-trend energy opportunities should be getting our

attention today?

Marin Katusa, who heads the Casey Research energy team, answers the

question by, correctly, cataloging the opportunities according to geography.

In North America

1. Geothermal -- the

most interesting of the alternative energy sources, by a wide margin.

2. Nuclear.

3. Oil.

In Europe

1. Unconventional gas has, by far, the

most upside.

2. Unconventional

oil.

3. Small hydro (such

as run of river).

In Africa

First and foremost, you want to avoid infrastructure

plays (pipelines, refineries, etc). Then you want to look for areas with huge

oil potential, which have been held off the market by concerns over political

risk. I like what Lukas Lundin is doing in Ethiopia, Somalia, and Kenya,

hunting for “elephants” with the idea of eventually selling the discoveries off

to the Chinese.

In Asia,

1. Liquid Natural Gas

(LNG)

2. Coal Bed Methane (CBM)

Lessons to Learn

There are a couple of

useful lessons to be derived by investors looking to tap into the virtually

unlimited opportunities in energy.

First, just because

something is “cheap” doesn’t mean it can’t stay cheap, regardless of historical

ratios -- if there has been a fundamental shift in the supply/demand equation.

Which is very much the case with North American natural gas.

Secondly, geological

and transport considerations make much of the energy complex a “local” market.

For example, while

North America enjoys an abundance of natural gas, Europe is forced to rely on

the heavy-handed Russians for the bulk of supplies. As you read this, there are

companies looking to break the Russian grip by applying the same unconventional gas technologies that

have so successfully built gas supplies in the U.S. -- technologies that are

only just now being applied in Europe. Early investors could reap huge profits.

In short, the real

opportunities are not found by simply “investing in energy” but rather by

taking the time to understand the structural differences within the energy

complex and cherry picking the special situations that invariably exist in a

sector this large.

David Galland is the managing director of Casey Research, LLC., a private

research firm providing independent analysis and investment recommendations to

individual and institutional investors in North America and over 100 other

countries around the globe. To learn more about the monthly Casey Energy Opportunities advisory,

including a special three-month,

fully guaranteed trial subscription, click here now.

By David Galland

Casey Research

July 25th, 2009