|

TUESDAY EDITION April 7th, 2026 |

|

Home :: Archives :: Contact |

|

|

Is US Oil Production Set to Plummet?Keith Schaefer, Editor Oil & Gas Investments Bulletin editor@oilandgas-investments.com November 11th, 2014 American oil production is set for a fast pullback, says Chris Theal, founder and CEO of Canadian energy fund Kootenay Capital. And that has two important implications

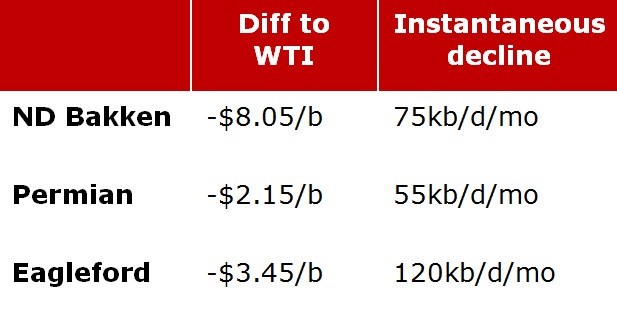

"We do think shale will rollover in output and it will be much sooner than most people think," says Theal. "We could very well see negative week over week contraction in output in the US before the OPEC meeting" on November 27. The oil rig count in the US has gone down four weeks in a row. It will be interesting to see how this shows up in the Wednesday EIA report on overall US production. Only 13 of the 42 weeks in 2014 so far have shown drops in US production. Theal and his team went back through weekly production data in the US starting after 2011-when tight oil production really took off. He says the data is more conclusive in the three instances when WTI fell below $85 a barrel; US output fell up to 200,000 barrels a day in literally a span of eight weeks-from a much lower production base than now. "If you see an initial roll in US output in the next few weeks it will be a major piece of data that the market will notice. The mentality is so negative that I think if you get some bullish data point like that you can see a fairly aggressive reversal" in oil pricing, Theal says. "If you get another drop in the rig count this week and a reversal in output-that's an instantaneous measurement of the Saudi objective." Umm...and...what's the Saudi objective? "Just put a governor on the pace of growth." Here's why he expects such a quick turn-down in US production: Producers in almost all the major oil basins in the US receive a discount to WTI. So they are receiving even less cash flow than many investors might think.

Bakken prices are $8/barrel below WTI, which closed at $78.68 Thursday. And that's what the oil marketers get. Producers get a $1-$4/barrel below that as their field price-so that's about $70/barrel or even a bit less. Theal says that realized price equals about a 10% return for industry-not enough. In fact, he estimates that the Top 5 North Dakota Bakken producers-Continental, Whiting, Oasis, Northern and Kodiak-have seen 2015 cash flow estimates fall by $870 million since oil prices dropped in the summer. That's $870 million that won't be going into the ground over the coming months. And with the high declines in tight oil production, the impact of that should be immediate. So that's the immediacy of dollars that aren't getting reinvested in the ground. The chart above uses a term called "Instantaneous Declines" which is how fast production would drop if ALL drilling in each basin stopped tomorrow. Of course, that is not going to happen, but Theal says that chart should give the Market an understanding of how much high-and-fast declines there are from "flush" production in the USA right now. Flush production is that high initial flow rate that falls off rapidly-65% or so-in the first year before flattening out to a 30%, then 25% then 20% declines in the following years. On their quarterly conference calls this week, several US producers were being very cautious about growth plans. Talisman (TLM-NYSE/TSX) said it would cut 2015 capex by $200 million. Rosetta Resources (ROSE-NASD) lowered spending by 20% and cut growth forecasts from 30% to 17-26%. Comstock Resources (CRK-NYSE) said it was committed to living within cash flow in 2015-which should mean a cutback in spending as their $510 million capex budget is $95 million more than estimated cash flows. Small cap Bakken operator Emerald Oil (EOX-NYSE) said it would drop a rig if oil prices stay sub $80/barrel. With the Saudis allegedly being firmly committed to keeping their production and market share up, that makes the high cost producer the swing producer-as logic would dictate they would cut back production first. That would be the USA, with its shale production. How does having a market based swing producer differ from when and how the Saudis managed the oil supply demand balance? "I think it makes a strong case for upside volatility being less pronounced; the oil price is now somewhat capped outside of geopolitical issues," Theal says. "There is a governor on how high it can go because at some price shale grows aggressively-like at $100/barrel. Everybody and their brother is drilling plays that can make hurdle rate economics at that level. He has already begun buying a basket of Canadian junior and intermediate light oil producers. If light oil does move higher, he doesn't think it's going to back to $100/barrel-which means investors increasingly need to avoid producers that require high oil prices to make their growth and/or dividend models work."I think there are a lot of businesses that rely on $100 crude…divco's and their models don't work at these prices."

Keith Schaefer, Editor The service we endeavor to provide is to analyze and clarify the nature and potential of certain North American junior oil and gas producers, and identify those situations where the market either misunderstands the nature of the company or assigns unduly optimistic or pessimistic success odds to the company. Keith Schaefer is not a registered investment dealer or advisor. No statement or expression of opinion, or any other matter herein, directly or indirectly, is an offer to buy or sell the securities mentioned, or the giving of investment advice. Oil and Gas Investments is a commercial enterprise whose revenue is solely derived from subscription fees. It has been designed to serve as a research portal for subscribers, who must rely on themselves or their investment advisors in determining the suitability of any investment decisions they wish to make. Keith Schaefer does not receive fees directly or indirectly in connection with any comments or opinions expressed in his reports. He bases his investment decisions on his research, and will state in each instance the shares held by him in each company.

|

| Home :: Archives :: Contact |

TUESDAY EDITION April 7th, 2026 © 2026 321energy.com |

|